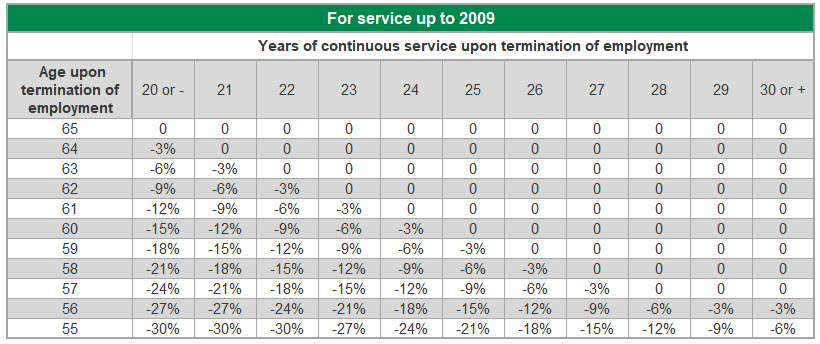

| Actuarial adjustment for early retirement

Percent of reduction applicable to an annuity payable at normal retirement age. For example, at Desjardins Group, the percentage of adjustment applicable on the portion of the pension payable at age 65, for the years of membership credited up to December 31, 2008, for a 58-year-old employee with 26 years of continuous service, is 3% according to the following table.

For years as of January 1, 2009, the adjustment is 4%/year for years missing between your age at retirement and age 62.

For service starting from 2009

|

Age upon termination of employment

| 65

|

64

|

63

|

62

|

61

|

60

|

59

|

58

|

57

|

56

|

55

| | Adjustment to the pension amount | 0 |

0

|

0

|

0

|

-4%

|

-8%

|

-12%

|

-16%

|

-20%

|

-24%

|

-28%

|

Actuarial certificate

Document signed by the plan’s actuary in which said actuary attests to the plan’s capitalization level, solvency and required level of financing (current contributions and deficit amortization where necessary).

Continuous service

The total number of continuous years as a regular employee or since the beginning of membership in the Plan, regardless of a temporary period of absence (e.g. parental leave). Any period of absence between two Desjardins Group employers is excluded.

Contributory earnings (for the purposes of the DGPP)

See Section 6-1 of the

DGPP Regulation.

Credited (recognized) service

SeeSection 5-1 of the

DGPP Regulation.

Death of a retiree with a dependent child A special measure of the DGPP provides that if the retiree still has dependent children upon death after retirement, the difference between the life annuity that was paid to the retiree and the one that will be payable to the spouse is paid to the child (or shared between the children) for as long as they are dependent children.

For example, at retirement, the retiree chose a 60% joint and survivor life annuity, with the spouse as beneficiary, guaranteed for 10 years; the amount of the annuity is $25,703. At the time of death, the retiree still has a dependent child. The DGPP will pay the spouse an annuity of $15,422 (i.e. 60% of $25,703) and an annuity of $10,281 payable to the dependent child (i.e. the difference between what the retiree received and what the spouse will receive upon the retiree’s death) for as long as the child meets the definition of a dependent child.

Deferred pension

To opt for a deferred pension means to leave your vested pension in the Desjardins Group Pension Plan (DGPP) upon a termination of employment. The value of the annuity is calculated using the salary for the best paid years and the number of years of recognized service that was credited at the time of the termination of employment.

Note: Should you be rehired in Desjardins and start contributing again to the DGPP more than 6 months after the end of your active membership date shown on the termination statement (more than 90 days if the termination was prior to January 1, 2020), you will be considered as a new DGPP participant. Hence, your credited service and salaries in your participation will not be considered in the calculation of your pension from your previous participation and vice-versa.

The deferred annuity will be indexed on January 1 of each year. in the first year, the indexation will be proportional to the period that elapsed since you left.

The indexation is based on that of the RRQ retirement pension. For service before December 31, 2008, indexation corresponds to that of the RRQ, subject to a maximum of 4% per year until you retire. For service as of January 1, 2009, indexation will be 50% of the CPI, subject to a maximum of 2% per year, up to age 55. However, for service starting on December 30, 2012, a pro-rated amount will apply to the first and last year of indexation.

Depending on the age at retirement, which must be between 55 and 65 years old, an actuarial adjustment will be applied. For the years until December 31, 2008, the actuarial adjustment will be determined according to your age and years of service up to termination of employment. The maximum adjustment equals ¼ of 1% for each month missing before your 65th birthday. However, if the “85 at age 57” rule indicates a lesser reduction, that percentage will apply. The “85 at age 57” rule = reduction of 0.25% per month to reach 85 and 0.25% per month to reach age 57. For years as of January 1, 2009, the reduction is calculated by actuarial equivalence.

For example: -

Termination: June 30, 2024

-

Gender: Male

-

Age: 46

-

Salary5 upon termination: $50,316

-

Salary8 upon termination: $49,352

-

MGA5 : $64,060

Years for the calculation of the value of the annuity:

-

Until December 31, 2008: 9 years

-

Between January 1, 2009 and December 29, 2012: 4 years

-

Starting December 30, 2012: 11.50 years

Deferred pension: $17,419

|

Pension calculation

|

Pension payable

|

|

Years of service

| | Pension credit 1

| |

Average salary | |

(Sum of 3 periods) |

Before 2009

|

9

|

X |

1.3% / 2%

|

X |

$50,316

|

= |

$5,887

|

From 2009 to 2012

|

4

|

X |

1.5% / 2%

|

X |

$50,316

|

= |

$3,019

|

After 2012

|

11.5

|

X |

1.5% / 2%

|

X |

$49,352

|

= |

$8,513

|

|

$17,419

|

¹ The pension credit gives a percentage (1.3% or 1.5%) of average salary up to average maximum pensionable earnings (MPE5) and 2% of average salary exceeding average MPE5.

Let us assume that this former employee wishes to receive their retirement pension at age 60, i.e. 14 years after having left Desjardins Group, and that the annuity indexation during those years is 2% for the years up until the December 31, 2008 and 1% for the years starting on January 1, 2009. The annuity payable under the plan, at age 60, will be $15,431, i.e.:

($5,887 X 1,0214) - 15%

|

=

|

$6,603

|

+ (($3,019 + $8513) X 1,019) - 30*%

|

=

|

$8,828

|

Annuity payable

|

=

|

$15,431

|

*The 30% percentage is approximate. This percentage may be less or more.

In addition, excess contributions calculated upon termination, plus interest, will serve to purchase an annuity that will be added to the previously determined annuity.

Dependent children

Any child under 18 considered to be your dependent is automatically covered if you are signed up for family or single parent healthcare coverage and/or spousal and dependent life insurance coverage. When a child turns 18, he or she may continue to be covered under the Plan if the following conditions are met:

-

The child must be a student. A student is an insured person aged 25 or less who is duly registered as a full-time student at an establishment recognized by the proper government authorities.

-

The child must not have a spouse, as defined under the Group Insurance Plan.

-

The child must be subject to parental authority exercised by you or your spouse, or would be subject to same if said child were a minor.

When dependent children reach the age of 26, they are no longer eligible for the Group Insurance Plan.

Please note that a person meeting the following definition is also considered to be a dependent person. The individual is of full age, without a spouse, living in the member’s or the member’s spouse’s household, and suffers from a functional deficiency as set forth by regulation under the applicable provincial statute, if applicable, and which is a deficiency that must have begun when the person’s condition corresponded to the provisions under bullet 1 or bullet 2 above; in addition, to be considered as suffering from a functional deficiency for the purposes of the insurance contract, the person must not receive any benefit whatsoever under a last resort assistance program provided by any provincial statute governing income support, and be domiciled with a person who would have exercised parental authority over him or her, had he or she been a minor.

Employee contributions

Contributions paid into the plan by the employee.

Contribution rate = 5.90% of the contributory earnings up to 65% of the

MPE and 9.30% on the surplus.

Example on a $30,000 salary: 30,000 X 5.90% = $1,770

Example on a $60,000 salary: ($44,525 X 5.90%) + [($60,000 - $44,525) X 9.30%] = $4,066.15

Excess contributions

Excess contributions are the result of a calculation required by law to ensure that your vested pension is at least 50% financed by your employer’s contributions. This means that if your cumulative contributions with interest represent more than 50% of the value of your pension, the difference is added to your entitlements as excess contributions.

Locked-in

The inability to fully withdraw money from a retirement plan, a LIRA or an LIF since the money is intended to provide retirement income.

Locked-in Retirement Account (LIRA)

In general, a LIRA is a savings account set up according to a written agreement between an individual and a financial institution authorized for that purpose, in order to accept and invest lump sums from a registered pension plan (RPP), until they are converted to a Life Income Fund (LIF) or a life annuity or transferred to another RPP. From a tax point of view, this agreement must meet the registration requirements for RRSPs as well as the rules specific to LIRAs and locked-in RRSPs. A LIRA is a product created by the Québec Supplemental Pension Plans Act (SPP Act). It is related to the locked-in RRSP governed by the federal Pension Benefits Standards Act (PBS Act).t

The Canada Revenue Agency (CRA) limits the amounts that can be transferred into a LIRA. If the value of your pension is higher than the limit set by the CRA, the amount that cannot be transferred to your LIRA will be paid back to you (income tax will be withheld). If you are 50 or less, the maximum pension value that can be transferred corresponds to your pension amount multiplied by 9. If you are between 50 and 55, this value increases gradually to reach 10.4 at age 55.

Maximum Pensionable Earnings

The MPE is the maximum annual salary on which a member contributes to either the Quebec Pension Plan (QPP) or the Canada Pension Plan (CPP). It generally varies each year.

In 2024, the MPE is $68,500.

|

Reference table for the main percentages associated with MPE |

MPE percentage

|

Corresponding amount

|

20%

|

$13,700

|

35%

|

$23,975

|

40%

|

$27,400

|

65%

|

$44,525

|

Maximum Pensionable Earnings of the last 5 years (MPE5)

The MPE5 represents the average of the last 5 years' Maximum Pensionable Earnings under the Quebec Pension Plan (QPP) for Quebec members, and under the Canada Pension Plan (CPP) for other provinces. In 2024, the MPE5 is $64,060.

Plan assets

All financial securities held by the retirement fund.

Retirement fund

Fund where contributions are deposited in order to pay retirement benefits and other benefits promised to members under the plan.

Spouse (for the purposes of the DGPP)

Important notes:

- The definition of “spouse” is not the same in the Desjardins Group Pension Plan (DGPP) and the Group Insurance Plan.

For DGPP members outside of Quebec, the provisions of the applicable provincial legislation take precedence over the Plan Regulation and may differ from those presented below.

The summary definition of a spouse for members living in Quebec for the purposes of the Desjardins Group Pension Plan (DGPP) is as follows:

The spouse is the person who is married to or united in civil union with the member and who is not legally separated from bed and board from the member.

If the member is neither married nor civilly united, the spouse is a person who has been living with the member in a marital relationship for at least 3 years or, in the following cases, for at least 1 year - at least one child has been born or will be born of their union;

- they have jointly adopted at least one child during their marital relationship;

- one of them has adopted at least one of the other’s children during this period.

If no one meets any of the above definitions, the spouse is a person whom the member has

designated in writing to the Desjardins Group Retirement Committee, and who has been living in a marital relationship with the member for at least 1 year.

Finally, if no one meets any of the above definitions, the member is deemed not to have a spouse for the purposes of the DGPP.

Supplemental Pension Plans Act (SPP Act)

The Supplemental Pension Plans Act governs the additional retirement plans of which private and municipal sector workers in Québec are members, as well as certain public sector plans. The Act is administered by Retraite Québec.

Tax withholding on refunds

All refunds in cash are subject to tax withholding in case of termination of participation. The applicable taxes withheld vary according to the amount of the refund as outlined in the following table. The exact amount of taxes payable will be determined when filing your income tax return for the year of the refund.

For participants living in the province of Québec:

|

Amount Refunded |

Provincial Tax |

Federal Tax

| Total Tax

| $5,000$ and less

| 14%

| 5%

| 19%

| Over $5,000 and up to $15,000

| 19%

| 10%

| 29%

| Over $15,000

| 19%

| 15%

| 34%

|

For participants living elsewhere in Canada:

Amount Refunded

|

Tax | $5,000 and less

| 10%

| Over $5,000 and up to $15,000

| 20%

| Over $15,000

| 30%

|

Value of the pension

The value is the amount of capital required at the time of valuation in order for there to be enough money to pay the promised pension at retirement. It is mainly influenced by pension plan features, your age, your gender, your salary and by economic parameters such as interest rates. The value of your pension is subject to substantial fluctuations. If you want to know the estimative value of your vested pension, you should refer to your annual statement which can be retrieved from your DGPP secure site. Please note that, for service from 2009, your contributions with accumulated interest provide a benefit of at least 175% in case of reimbursement of the value of your pension. If applicable, your entitlements are paid in proportion to the Plan's solvency ratio.

|